Long-Term Disability Insurance

Blog content provided in partnership with Benjamin Yin, MBA, Owner of Generational Financial Partners LLC.

Navigating Your Benefits

The benefits of working as an independent contractor physician are immense. In addition to receiving special tax incentives, independent contractors also have greater control over financial earnings, customized investment options and, one of the most important, more options of insurance carriers, plan types and coverage limits.

As a physician, your biggest asset is not your house, car, 401(k) or your investments. Your biggest asset is the ability to earn a healthy income. One of the best ways to protect yourself and your income is by purchasing a long-term disability insurance policy.

Use this article as a brief overview of long-term disability insurance for independent contractors; the benefits, the options and the importance.

Definition

Long-term disability insurance is a policy used to protect an individual from loss of income in the event he or she is unable to work due to accident, illness or injury for an extended period of time. This policy typically begins to assist after the individual has experienced a loss of income for more than 90 days (or three to six months).

Generally, a policy pays up to 60% of the individual’s annual salary until he or she is 65 years old, although every plan is different. Disability insurance premiums are not tax deductible but benefits are received tax-free if a claim is made.

Overview

The details are not always clear with disability insurance, making it one of the more confusing insurance policies to navigate. Compared to life insurance policies which are very clear cut, long-term disability policy options and features are scenario-based which creates a grey area when determining what is covered, and more importantly, what is not covered. Those grey areas often prompt two main questions:

- Who determines if you are disabled, or not?

- Is it the client (person insured)?

- Is it the insurance company/provider?

- Is it the client’s physician?

- Is it the insurance company’s physician?

- What definition is used to determine if you are disabled, or not?

- Who creates the definition?

- How is it determined?

The answers to these questions are within the policy details. As an independent contractor physician, you pick all of your own insurance carriers and plans. Although it sounds challenging to navigate what you do and do not need, this is a huge benefit.

This means you are not subject to one specific insurance carrier for all insurance types. You choose the plan, the carrier and the features to best meet your unique needs, eliminating the grey areas which are often present when enrolled in a group policy. There should be no questioning who determines if you are disabled and how disability is defined when you are working one-on-one with an insurance carrier to pick your plan.

In addition, your plan is not impacted by a larger group. Only your illnesses, habits and activities impact the policy – not someone else’s. You determine the amount of coverage you want or need. There is no need for two policies to receive adequate coverage. An individual policy is simple – one carrier, one plan.

Top Five Carriers

Top Five Carriers

When it comes to purchasing individual disability insurance, all carriers are not made equal. There is no one-size-fits-all, long-term disability insurance carrier. As a high-income earner, researching the top-rated carriers is important. In no particular order, some of the top-ranked, long-term disability insurance carriers include:

- Guardian

- MassMutual

- Principal Financial Group

- The Standard

- Ameritas

These carriers are the most commonly recommended providers for high-income earners and independent contractors across a number of varying specialties. When choosing the best option for your individual situation, consulting with an experienced financial advisor is recommended to discuss each carrier and plan offering in detail.

Type of Plan Riders & Features

Even among the list of top carriers, disability is defined differently. One way to tailor the definition of disability to best meet your individual needs is to customize a plan through riders and features.

Riders are provisions to an insurance policy that amend the basic policy language to add benefits or additional coverage. There are a number of riders or features to consider. Examples of the most common include:

1. True Own Occupation

True Own Occupation defines disability as the inability to work your regular occupation, regardless of the ability to work another job. Under true own occupation, benefits are to be paid no matter what else you are qualified to do or decide to do. Interpretations of occupation differ across all carriers.

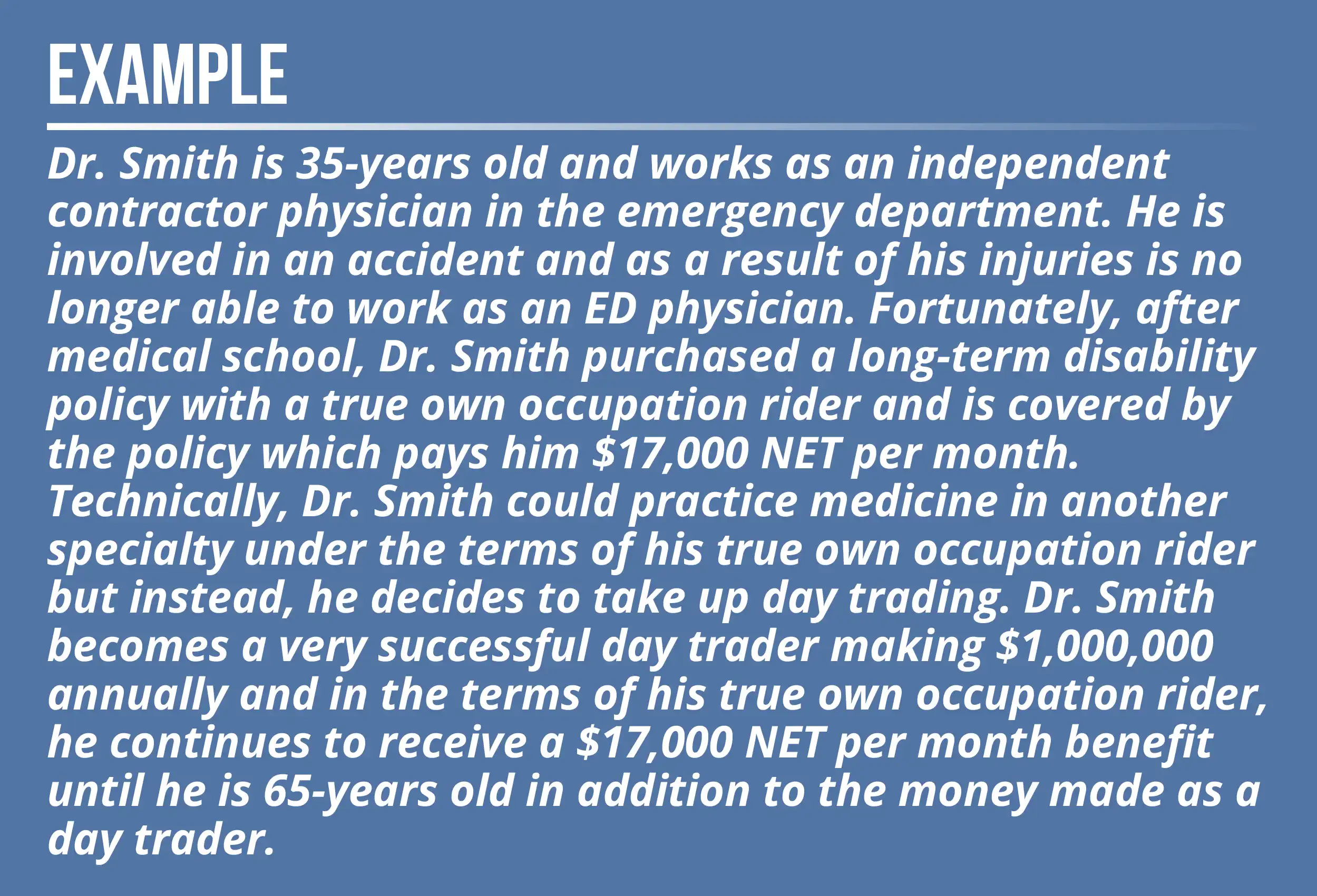

As a physician, some carriers allow you to list your specialty of medicine as your occupation. For example, the occupation listed in the policy would state emergency department physician instead of physician. This specification would not limit you from practicing as a physician in another medical specialty in the event you become disabled.

True own occupation scenarios differ from carrier to carrier. Some carriers will state a disabled person is eligible as long as the total income does not surpass the amount of income previously made. In the example with Dr. Smith, he would not receive the $17,000 per month benefit if he was averaging $1,000,000 per year as a day trader. However, he could receive the $17,000 per month working a job with a salary less than his physician salary.

Some policies include true own occupation in the basic language while others offer the rider at an additional expense. It is important to remember the stronger disability is defined, the more expensive a policy will be.

Some policies include true own occupation in the basic language while others offer the rider at an additional expense. It is important to remember the stronger disability is defined, the more expensive a policy will be.

2. Residual or Partial Benefit

Most disabilities are not outright catastrophic. While catastrophes happen, most disabilities are considered partial. In this case, a residual (or partial) feature is beneficial. A residual feature pays partial benefits if you experience a loss of time or duty in comparison to your work-life prior to the claim.

Similar to true own occupation every carrier uses a different scenario or definition to determine when a person receives benefits.

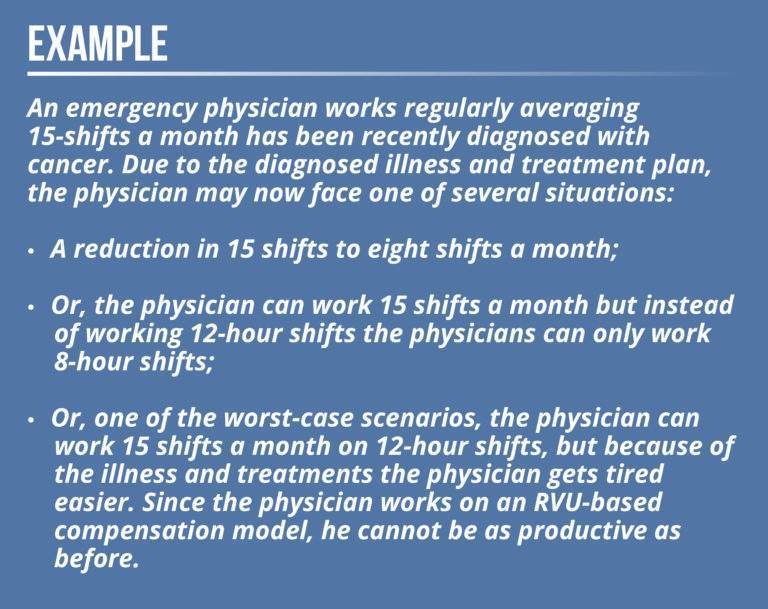

One policy will state if there is a deduction of income greater than or equal to 15%, some benefits will be offered. Another policy will require a loss of income greater than or equal to 20%, as well as proof of loss of time or duty. When you have fewer shifts or are no longer able to do something you were before, it is easy to file a claim and provide proof.

However, as stated in the worst-case scenario, the physician did not lose time or duty but instead experienced a loss of productivity. As a result, the physician cannot see as many patients as before and is making 15-20% less income. This scenario can be more difficult to prove if it is not mentioned when purchasing a plan. In all three scenarios, the best policy will pay a benefit in the event of a claim. As always, the strongest definition will be the most expensive.

3. Catastrophic Rider

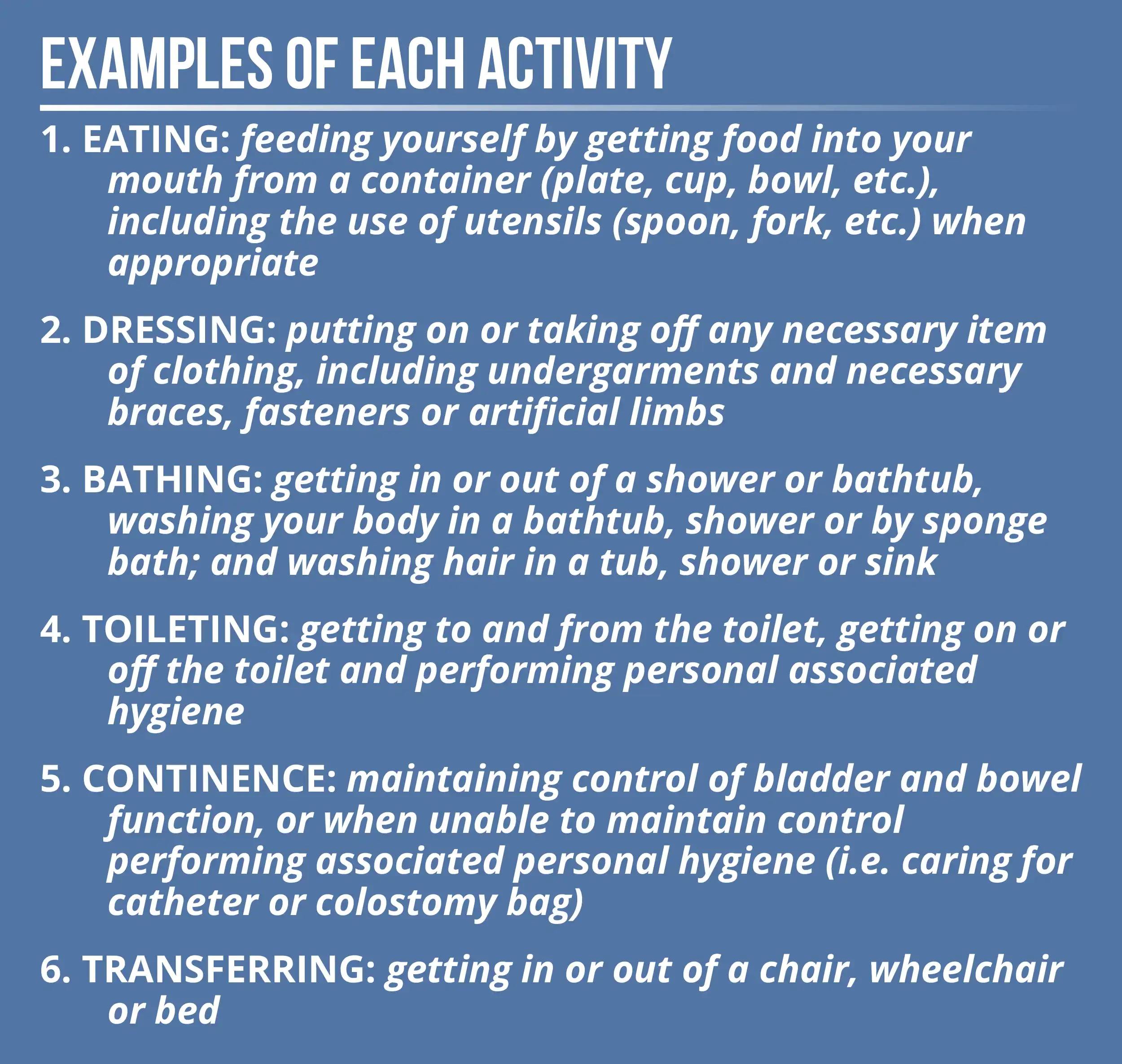

A catastrophic rider provides benefits in the event an individual becomes disabled and needs assistance with two of the six activities of daily living.

In addition to receiving a benefit of up to 60% of your annual salary, the rider may include an additional benefit amount set by the insurance carrier (up to an additional $8,000 per month in disability benefit). The purpose of this benefit is to provide supplementary financial assistance for expenses you may incur as a result of a disabling injury or illness (i.e. in-home nursing assistance, additional therapy, etc.).

Under this rider you are also eligible for coverage if you experience a total or permanent loss of vision or hearing or experience cognitive impairment (loss of mental capacity). Catastrophic riders are one of the least expensive plan riders to add to a policy.

4. Cost of Living Adjustment Rider

A cost of living adjustment (COLA) rider is added to a policy to help offset the risk of inflation in the event you become disabled. This rider will increase benefits annually, typically starting after you are disabled for 12 months. The benefit amount will only increase when a claim is active and does not make up for the time period between the purchase of the policy and when you file your disability claim.

The purpose of this rider is to secure and protect the value of your benefit. Without the COLA rider, your benefit amount will stay the same for the length of the benefit period, meaning the amount you receive will have less purchasing power 15 years after a claim is originally filed.

Two common ways insurers factor benefit increases are a fixed percentage (typically 3% annually) or a third-party index (i.e. Consumer Price Index). Fixed percentages remain unchanged for as long as the benefit period is active. If the index increases, the benefit increases when using a third-party index. Usually, benefits based on a third-party index set a minimum (1-2%) and a maximum cap (approximately 6%).

5. Student Loan Protection Rider

Medical school is a major financial commitment. Following graduation and training, a large portion of most physicians’ monthly budget is contributed to paying off student loan debts. Student loan protection is an optional rider which provides additional coverage to the benefit amount to cover the cost of student loan payments. Provisions of a student loan protection rider differ from carrier to carrier.

Unfortunately, if a disabling injury or illness occurs, these debts still have to be paid. This rider is beneficial if your maximum disability benefit falls short of your monthly expenses, or if you have a student loan payment more than the rider minimum to be paid within 10 to 15 years.

Not all physicians need the student loan rider, especially if you have federal loans. It is recommended to review student loan protection riders with a professional to help assess your individual needs.

Time to Purchase & Exclusions

Purchasing a policy is always less expensive when you are young and healthy. This is the time to purchase as much coverage as you can afford to lock in insurability. Typically, this is also when the best discounts are offered. For example, a carrier might offer a discount to a young, healthy physician who is training in a residency program.

Discounts last throughout the life of your policy, so when you increase coverage later you get to keep the discount. When you have student debt and are just starting your career you do not have as much in savings, so a disability can change the rest of your working life and your ability to earn a healthy income.

As you get older, the need for disability insurance decreases. You’ve likely spent more time saving and aren’t as focused on building a career and paying off debt, so all of the riders and features aren’t as necessary. Once you purchase a policy, coverage can be adjusted to include only what you actually need.

Exclusions are another reason to purchase early. Pre-existing medical conditions, activities, hobbies, vehicles, etc. can all be excluded from coverage. Two of the most common exclusions for physicians nationwide are musculoskeletal (MSK) disorders and mental health.

Get the policy before life happens. Once you are approved for coverage anything after the signed date cannot be used against you.

Examples of plan exclusions:

- If you ride a motorcycle, your policy can state anything relating to a motorcycle injury is not covered.

- If you’ve been treated for back pain, your policy could state any condition or future injury related to the pre-existing condition is excluded.

- If you take medicine for anxiety, attention deficit disorder (ADD) or depression, your policy will not cover disability as a result of these pre-existing conditions.

The Importance

Physicians are in the top 1-2% of income earners in the nation and some of the most likely to experience a work-limiting illness or injury due to the specialized skill set. With an income much higher than the average American, a disability would be catastrophic without the proper protection.

Unfortunately, government funded programs (i.e. Social Security) would not begin to cover the cost of a mortgage, utility bills, car payments, student loan debts and all of life’s other expenses. For the most part, if you are disabled these expenses still have to be paid. A strong, long-term disability policy insures protection of your most valuable asset – your income.

Schedule a free 15-minute call with trusted partner and financial advisor, Benjamin Yin, Owner of Generational Financial Partners LLC, to further discuss the importance of long-term disability and how to customize your policy as an independent contractor physician.

_____________________________________________________________________________________________________

Described in this document is one of the many advantages of being paid as an independent contractor (IC) versus being paid as an employee. The scenarios provided in this document regarding tax savings, long-term disability insurance and retirement planning strategies are neither recommendations nor suggestions, but are merely examples of how in specific cases it can be very advantageous for a physician to be paid as an independent contractor. We recommend before employing any of the strategies discussed each provider obtains the guidance and advice of an experienced financial planner and a knowledgeable accountant to determine a specific strategy which most effectively meets the physician’s individual needs.

Please correct the following fields before submitting:

- Field Name is required

- Field Email is required