Employee vs. Independent Contractor

Employee vs. independent contractor – what is the right fit for you? Hospitals and health systems nationwide partner with physician services groups to operate and provide coverage for emergency departments versus employing physicians on their own. This commonality often leads physicians to the question of which employment model is better – employed (W-2) or independent contractor (1099)?

In general, one employment model is not “better” than the other. The two are very different. To compare, focus on what is best for your circumstances. Some physicians are more comfortable with employed models and company-provided benefits. Others are more comfortable with an IC model and enjoy complete control of personal finances and benefit selections.

There are many variables to consider when determining which model best meets your needs. Use this blog post as a basic comparison to help define the statuses, benefits and incentives. Keep in mind – research is key and it is best to speak with a financial advisor and certified public accountant (CPA). You may be surprised which employment model maximizes your total income.

Definitions

The first step in determining the perfect fit for you is to understand the differences between the two models. The two IRS definitions are listed below.

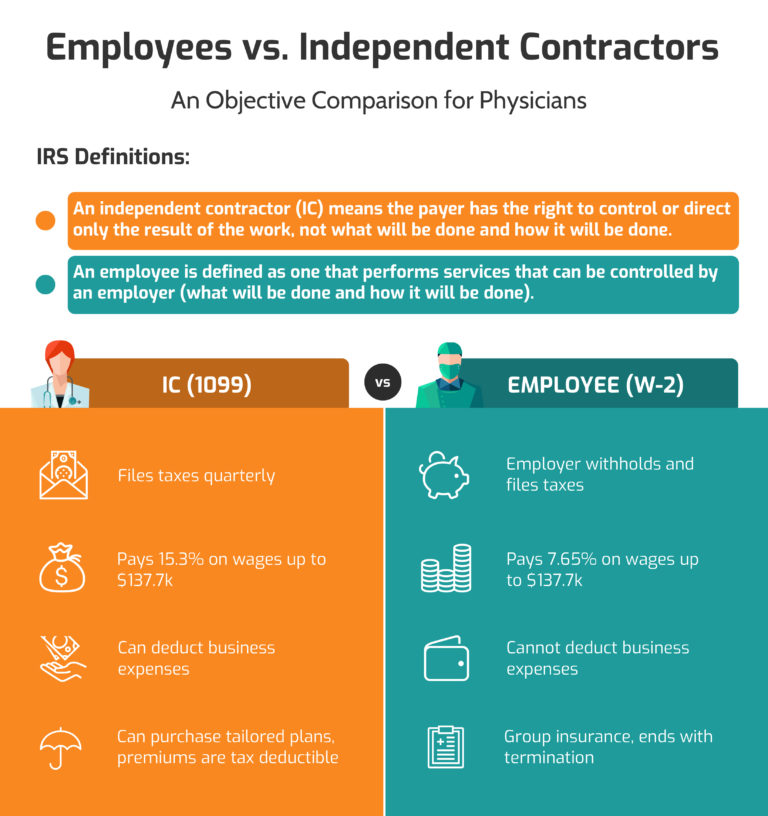

- An individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done.

- An employee is defined as one that performs services that can be controlled by an employer (what will be done and how it will be done).

The Basics

IRS Classifications

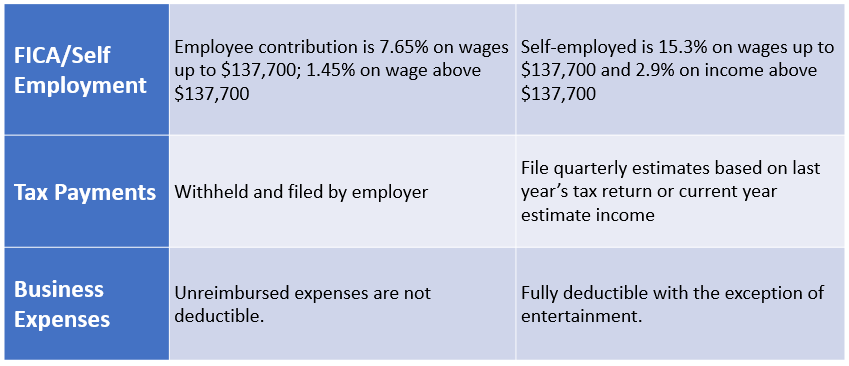

The earnings of a person working as an IC are subject to Self-Employment Tax, meaning you pay the combined employer and employee amount. For 2020, it is 12.4% Social Security tax on up to $137,700 of your net earnings and 2.9% If your income is more than $200,000, or $250,000 for married couples filing jointly, you must pay 0.9% more in Medicare taxes.

Those considered employees are not subject to self-employment tax but may be subject to The Federal Insurance Contributions Act (FICA). Both you and your employer pay 6.2% Social Security tax on up to $137,700 of your earnings and a 1.45% Medicare tax on all earnings.

Self-employed persons will take a deduction for the 6.2% employer’s share of Social Security along with 1.45% employer’s share of Medicare as an above-the-line deduction.

Tax Payments

Federal Insurance Contributions Act (FICA) is how self-employment taxes are collected. As an employee, all tax payments are withheld and filed by the employer. As an IC, the individual files quarterly estimates based on last year’s tax return or current year’s estimated income.

Business Expenses

Business expenses are the cost of carrying on a trade or business and are usually deductible if the business operates to make a profit. As an independent contractor, all business expenses are fully deductible except for entertainment expenses. For employed physicians, unreimbursed business expenses are not deductible. A list of deductible expenses and further instructions are provided on the IRS website.

Federal Tax Rate

Understanding tax brackets can have a huge impact on your finances and how to maximize tax returns. To figure out what bracket you fall under, look at last year’s tax return and calculate what your effective tax rate was. Some online calculators will do this for you.

Hours and Compensation

Whether you are an IC or an employee, you will need to consider hours and compensation rates to properly compare which status is best for you. Several questions to explore include:

- Are you compensated hourly or on a base rate schedule?

- If a base rate, what is the average annual compensation focused on wages (no benefits, insurance, etc.)?

- If an hourly rate, what is the minimum number of hours needed to be considered a full-time employee? Are you able to increase hours if needed?

- Are you paid a flat rate regardless of how efficient you are (number of patients seen)?

- Is there an opportunity to increase your base rate by seeing more patients?

- How are more efficient physicians incentivized in your model?

- Is there a quality-based component to the payment structure?

When comparing the income values of both, employers almost uniformly overestimate the value of the benefits being provided by their organizations. An easy way to compare the compensation packages is to figure out how much each benefit is worth on annual basis, then divide by the average number of hours you will work per year which equals an estimated hourly value of each benefit. Then, add the value of the estimated hourly benefit to the hourly employee compensation rate.

For example, if an employer provides healthcare insurance and an equivalent healthcare plan could be obtained for $600 per month ($7,200 per year), and you plan to work 1800 hours per year, the hourly value of this healthcare benefit is $4.00 per hour.

Malpractice/Tail Insurance

Malpractice/Tail Insurance is another important benefit to focus on when comparing job opportunities and employment statuses. Several questions you should ask:

- Is malpractice/tail insurance provided?

- What types of policies are in place (claims made vs. occurrence based)?

- What is the group’s malpractice history?

- How does the group/organization defend their physicians?

The Benefits

Often, what attracts physicians to an employed model is the feeling of getting the “entire package.” In some cases, this results in a lower wage because of the employer overvaluing the cost of the total rewards package offered. This is not always accurate, but it is worth researching what an employer would include versus what it costs to pay for it yourself.

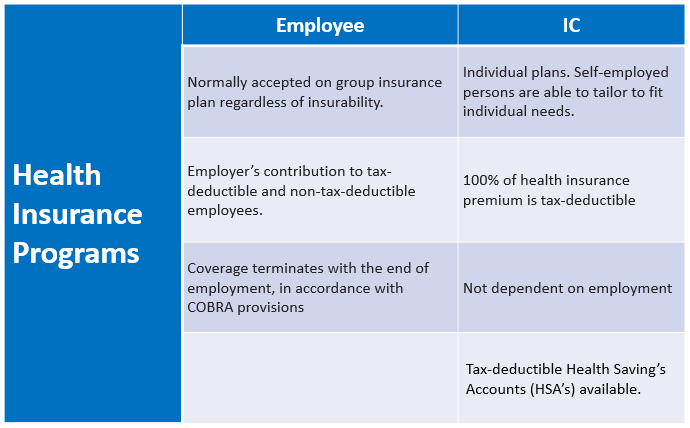

An employer’s benefits package may not include everything you need adding additional expenses to your wallet. Be sure to thoroughly research what is offered. You may be surprised there is not much of a difference in purchasing customized plans as an IC. Packages to consider include:

- Health Insurance

- Vision and Dental Insurance

- Long-term & Short-term Disability

- Life Insurance

- 401(k) or Another Retirement Plan Option

- Continuing Medical Education

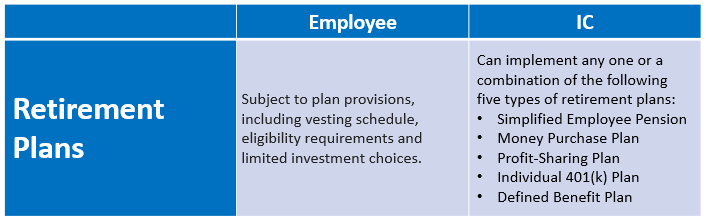

Retirement plan options and disability insurance are two very important plans for physicians to research and compare. Make sure your assets are protected in the event you are not able to work. Also, when you are ready to retire, your investments should allow you to live and spend at a comfortable rate. Use the chart below for a quick comparison of retirement plan options between the two models.

The Incentives

Finally, make sure you know and understand all the factors surrounding any incentives or productivity bonuses. At-risk bonuses are challenging to predict as they are highly variable and can hinge on factors beyond your control. Get a sense of what the average payout per physician is at each facility for these bonuses and ask specific questions on what levels are needed to achieve bonuses.

Keep in mind – research is key. It is best to consult with a trusted certified public accountant and a financial advisor who is experienced in maximizing finances for independent contractors. You may be surprised which employment model maximizes your income, benefits and incentives. Click here to learn more about the benefits of practicing as an independent contractor.

Blog originally posted: 9/18/2017 | Updated: 4/17/202

The information provided is not written or intended as tax or legal advice and may not be relied on for purposes of avoiding federal tax penalties. Described in this text are some of the many advantages of being paid as an independent contractor (IC). The scenarios provided regarding tax saving and retirement planning strategies are neither recommendations nor suggestions but are merely examples. Individuals are encouraged to seek advice from their own financial advisor, CPA and/or legal counsel.

Please correct the following fields before submitting:

- Field Name is required

- Field Email is required